Because of its federal structure, there is no uniform tax rate in Switzerland. Average tax rates can't be calculated because of the multi-layered tax system. Taxes are calculated based on specific figures for specific cantons and municipalities.

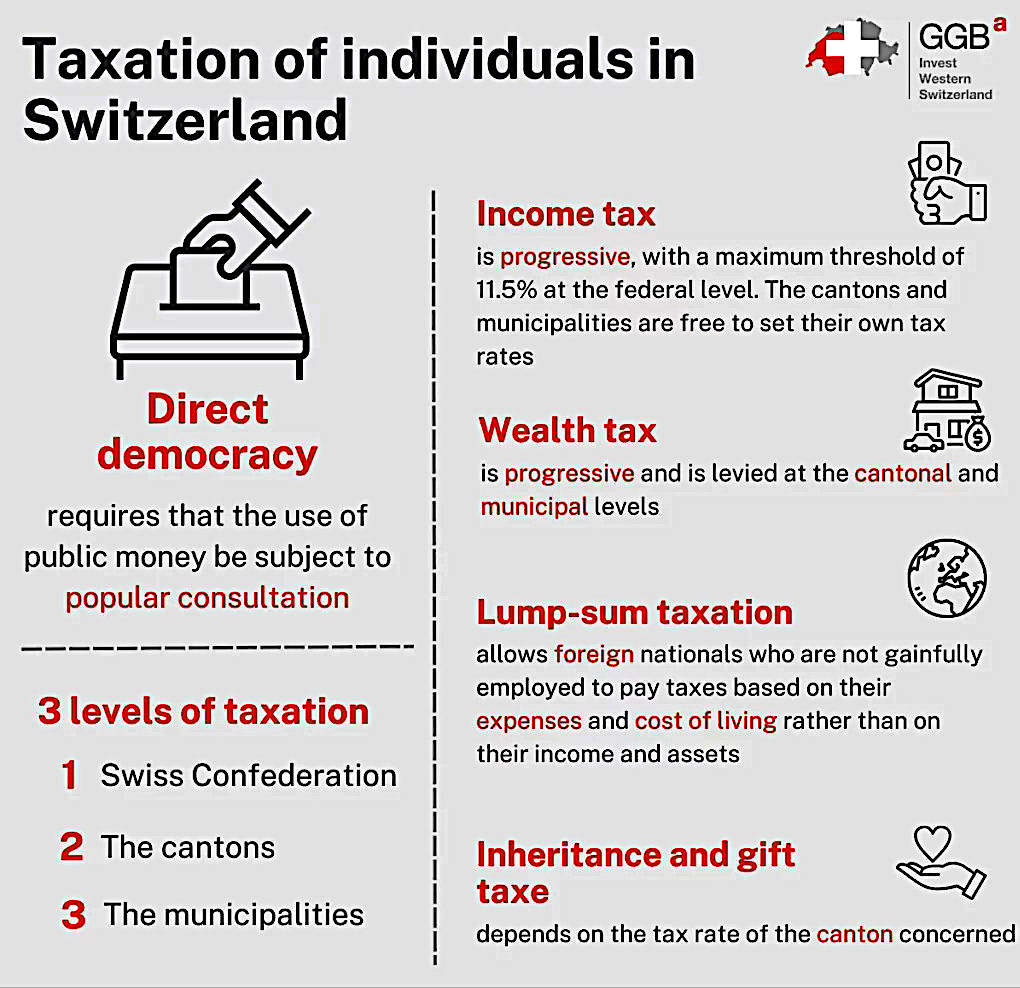

Democracy also applies to taxes: Swiss citizens vote on what taxes they have to pay. They can also have a say in determining the tax rates and the tax co-efficient.

The Swiss tax system is based on three levels of taxation:

Federal level: Tax is levied at the national level on income and corporate profits.

Cantonal level: Each canton applies its own tax rates, meaning that taxation can vary significantly by region; the tax rates must be agreed by the citizens.

Communal level: Municipalities apply a coefficient to the cantonal tax rates to determine their own taxes; the coefficient is determined by the citizens.

All taxes are collected at the municipal level ie. tax is paid in at the bottom level and applicable portions pushed up to the next levels, not as in most other countries where tax is paid in at the top level with the expectation that a portion will filter down to the bottom level.

Cantonal and muncipal taxes

Each of the 26 cantons has a separate law for their own cantonal taxes which their citizens determine in accordance with the Federal Tax Law.

Municipal taxes are levied as a multiple of cantonal taxes.

Because each commune (municipality) determines its own tax co-efficient, these can vary considerably so there can be low-tax and high-tax communes within the same canton.

Tax laws and tax rates vary widely among cantons and among municipalities, so choice of residence is an important element of tax planning.

The various cantonal and municipal taxes are levied at progressive rates. The percentage of taxable income that an individual has to pay in cantonal and communal taxes is determined by the statutory tax rate set by law and the applicable tax co-efficient, which is changed from time to time.

There are also cantonal and municipal taxes on personal net wealth; rates vary per canton resulting in an overall personal net wealth tax rate between 0.01% and 1.03%.

Equalization Fund distributes the wealth equitably

In order to prevent differences in the tax income creating pockets of rich urban areas surrounded by poorer farming areas, there is a National Equalization Fund whereby financially strong cantons pay into an Equalization Fund and financially weak cantons receive payments. This distributes the tax wealth generated in the country equitably and fairly.

On the local level, as part of their commitment to solidarity with their fellow citizens, wealthier communities "twin" with poorer rural communities and help support them to ensure that their local facilities are kept at a similar standard and that the same quality of schooling can be offered to all children, regardless of where they live. This greatly helps to prevent movement of people away from the rural areas as they are assured that there is little difference in schooling quality - and the quality of rural life is so much healthier.

Taxation for Individuals

Income and total wealth are taxed; rates vary by canton and municipality which leads to significant differences in tax burdens across regions and even between neighbouring municipalities.

Income tax is progressive, so the tax rate increases with income.

Each canton applies its own scales and rates, leading to notable variations although most are competitive rates.

Wealth Tax is levied at the cantonal and communal levels and applies to the net value of assets held by an individual, after deducting debts. Rates and exemption thresholds vary by canton.

Example of individual income tax

Married taxpayer, two children, gross salary income of CHF 150,000 (= high earner) - would pay the following income taxes depending on where he/she lived (all figures are in Swiss Francs):

Canton/

|

Federal

|

Canton &

|

Total

|

|---|---|---|---|

| Zug | 1'058 | 1'663 | 2'721 |

| Lucerne | 1'058 | 9'734 | 10'792 |

| Lausanne | 1'058 | 14'010 | 15'068 |

| Geneva | 1'058 | 2'740 | 3'798 |

| Zürich | 1'058 | 8'557 | 9'615 |

Corporate Tax

Companies pay a Federal Corporate income tax of 8.5% on profit after tax and on capital. Cantonal and communal taxes are added to the Federal tax, resulting in an overall effective tax rate between 11.9% and 20.5%, depending on the company's location of corporate residence in Switzerland.

Federal taxes

At the federal level, only about 30% of the Federal government's income derives from income tax. Its main sources of income are customs duties and taxes on consumption - VAT (sales tax), tobacco, alcohol, casino taxes, mineral oil tax, the rates of which are determined by the National Council and Council of States (Parliament/Congress) who also decide on the federal budget.